Cadmium telluride solar photovoltaics (PV) are a key clean energy technology that was developed in the United States, has a substantial and growing U.S. manufacturing base, and holds more than a 30% share of the U.S. utility-scale PV market. The Cadmium Telluride (CdTe) PV Perspective Paper (PDF) describes the state of CdTe PV technology and provides the perspective of the U.S. Department of Energy (DOE) Solar Energy Technologies Office (SETO). It presents SETO’s priorities to advance CdTe technology through investments to reduce costs, address materials availability and supply chain costs, and support the ongoing scale-up of CdTe technology within the domestic utility-scale PV market. These priorities will enable CdTe PV to support SETO’s goal of improving the affordability, reliability, and domestic benefit of solar technologies on the electric grid.

Over the past two decades, CdTe PV costs have fallen, efficiencies have increased, and manufacturing economies of scale have been realized. CdTe provides inherent manufacturing advantages over its main competitor, crystalline silicon (c-Si) PV, including lower energy consumption and lower capital costs for scale-up. However, c-Si PV technologies are currently more efficient at both the cell and module level.

CdTe PV can become more competitive with c-Si PV by accelerating technology innovations to reduce cost, increase efficiency, boost availability of materials, and improve end-of-life (EOL) management, while ensuring there is a skilled workforce to realize this progress. In addition, since CdTe represents a significant share of U.S. utility-scale PV deployment, tools for system characterization, monitoring, operations, and maintenance that were originally designed for c-Si PV must be able to accurately assess the performance of CdTe technology. Together, these improvements can enhance CdTe PV’s performance, reliability, and bankability. SETO has identified the areas described in this report as top priorities to support the present and future competitiveness of CdTe technology.

CdTe Industry and Technology

At present, CdTe is the leading domestically fabricated PV technology (by volume) and plays a key role in the expansion of PV deployment and employment in the United States. In 2022, CdTe technology commanded about 34% of the U.S. utility-scale PV market and about 3% of the world PV market, and preliminary 2023 data is currently indicating flat CdTe module shipments year over year.1234 The historical market share of the CdTe module technology in the U.S. utility-scale market segment over the past 10 years is shown in Figure 1. Effectively all CdTe modules are currently used in utility-scale PV systems, as rooftop PV systems have more constraints on system size and efficiency needs that make silicon modules more favorable.

Domestic production of CdTe PV modules supports the U.S. economy, creates jobs, and provides technological diversity to the PV industry. The CdTe PV supply chain is fundamentally different from c-Si PV, with materials and tools within it often sourced from firms in the United States or our allied nations, in contrast to c-Si. As manufacturing of CdTe PV continues to expand, this expansion also helps drive U.S. economic growth.

CdTe has many desirable attributes, including high durability, low embodied energy (the sum of all energy used in its production), a fast production process, and established bankability.6 In contrast to silicon solar modules, which comprise discrete solar cells arranged in strings, CdTe modules are monolithically integrated and directly deposited on single flat sheets of glass. The streamlined manufacturing process of CdTe photovoltaics can offer certain advantages over that of silicon: an 18.5% efficient CdTe module has about 35% the embodied energy compared to a single-crystal silicon module of the same power rating (144 half-cell bifacial silicon passivated emitter and rear contact module with 21% efficiency). One recent paper indicated that the additional embodied energy associated with manufacturing a silicon PV module would take roughly four additional months of module operation to pay back as compared to a CdTe module.7

Performance of the best R&D CdTe PV cells is currently lower than that of the best silicon cells. The highest-certified CdTe cell efficiency currently stands at 23.1% and was set using a 0.45 cm2 cell area. The highest-certified silicon cell efficiency is currently 27.3%, set using a 243 cm2 cell area.8 The ability to make industrially relevant cells with high-power conversion efficiency is vital in order to provide headroom for commercial module power output to continue to grow and for the CdTe technology to remain competitive with a rapidly scaling silicon PV supply chain. Worldwide, while c-Si PV has over 1,000 GWdc installed, this compares with around 30 GWdc installed capacity for CdTe PV.9,10

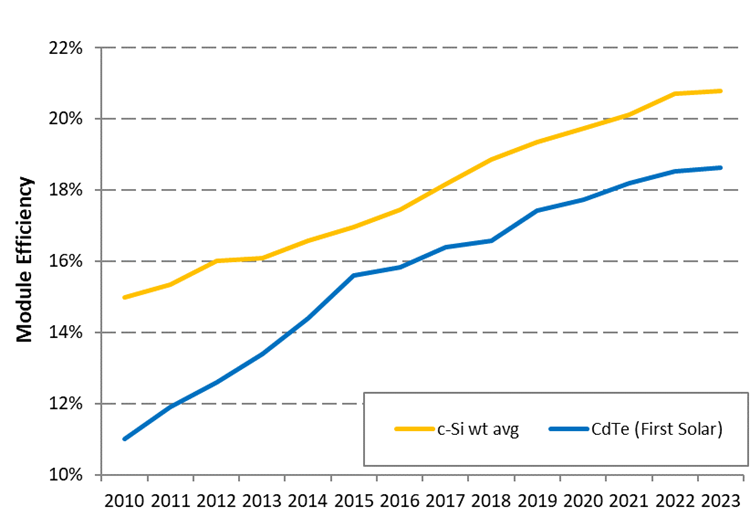

Fleetwide averages of CdTe module efficiency have historically remained within a reasonable margin of monocrystalline silicon modules, as shown in Figure 2. There is significant uncertainty in what will happen in the next few years as the silicon supply chain completes its transition to n-type tunnel oxide passivated contact and heterojunction modules, which could result in a dramatic increase in fleetwide module efficiency levels. The record efficiency of the highest-performing silicon module is 24.9%, while the record efficiency for CdTe modules is notably lower at 19.9%.8 It will be necessary for CdTe module performance to continue rising for CdTe PV technology to remain competitive in the long term.

There is only one CdTe company manufacturing at gigawatt scale: as of September 2024, First Solar had a 9.4 GWdc-per-year domestic manufacturing capacity accounting for all U.S. CdTe PV module production, and by 2025 over 20 GWdc from factories in the United States, India, Malaysia, and Vietnam

Figure 2: Fleet average efficiency values estimated from published information from the State of California (monocrystalline and multicrystalline silicon) and First Solar (CdTe). The highest-performing CdTe modules are currently made by depositing CdTe onto low-iron float glass with a fluorinated tin oxide transparent conductive oxide (TCO) layer. The combined cost of the front and rear glass sheets can make up 15–20% of the total cost and a large fraction of the embodied energy of a completed CdTe module. Nippon Sheet Glass Group is the preeminent supplier of this commodity, with a large factory (inaugurated in 2020) located near both First Solar and Toledo Solar in Lucky, Ohio. Recently, Vitro Architectural Glass agreed to supply TCO-coated glass to First Solar, expanding and upgrading their Carlisle, Pennsylvania plant.14

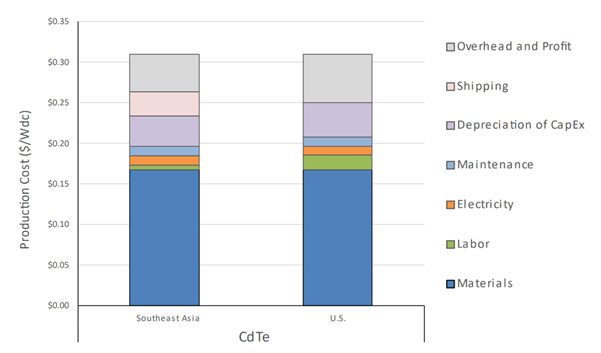

Supporting the growth, diversity, and scale of the domestic CdTe supply chain could reduce the production cost and increase the cost competitiveness of CdTe modules. A breakdown of estimated CdTe PV production costs is provided in Figure 3, with material costs making up a majority of the final cost of goods sold. There is significant uncertainty in the cost modeling of CdTe module production since actual supply chain costs are proprietary to a single company. However, a useful takeaway from this analysis is that CdTe module production costs in the United States appear to be competitive with production in Southeast Asia, especially considering the impacts of the IRA and the additional shipping costs associated with delivering modules from Asia to the United States for deployment.

Dramatic cost reductions across the silicon supply chain have exerted intense downward price pressure to CdTe modules, which compete directly with silicon modules in the utility-scale PV market.15 However, the cost competitiveness of domestic CdTe modules relative to imported silicon modules has been protected by trade policy, including tariffs on imported silicon solar cells and modules under section 201 of the Trade Act of 1974 (extended in 2022), anti-dumping and counter-vailing duties against silicon cells and modules from the People’s Republic of China and Taiwan,16 and tax credits for domestic PV manufacturing and domestic content through the IRA of 2022. In particular, the Advanced Manufacturing Tax Credits from the IRA have the potential to dramatically reduce the minimum sustainable selling price of U.S.-produced modules17 and should provide a significant increase in competitiveness for domestic CdTe manufacturing. Additionally, U.S.-manufactured CdTe modules already have a domestic content of 60–90%, while U.S.-manufactured silicon modules often have a greater reliance on imported components. Given their relatively large domestic content and growing U.S. manufacturing base, CdTe modules are expected to be well positioned to contribute toward the domestic content bonus credit for the Investment Tax Credit and the Production Tax Credit for system developers and owners.

Figure 3. Modeled market price aggregated by cost category for CdTe PV modules produced in Southeast Asia and in the United States.

SETO CdTe Portfolio and Research Community

SETO has employed several programs to support the competitive position of CdTe PV.18 This includes opportunities for cooperative funding agreements and grants for university and national laboratory research and development, as well as industry-focused research, development, and demonstration funding programs. Fiscal year 2020–2023 programming that supported CdTe innovation included multiple PV funding opportunity announcements (FOAs), Small Innovative Projects in Solar (SIPS) FOAs, Incubator FOAs, the Small Business Innovation Research/Small Business Technology Transfer Research funding program, the Technology Commercialization Fund funding program, and the American Made Solar Prize, as well as the CdTe Accelerator Consortium (CTAC) and National Renewable Energy Lab (NREL) core program for CdTe research.19,20,21

SETO’s current and historical investments have supported CdTe PV innovation for levelized cost of energy (LCOE) reduction through improved power conversion efficiency (PCE) and manufacturing throughput, reduced module embedded energy, higher fielded module energy yields, and enhanced module recycling technology for the reclamation of valuable raw materials (and containment of their toxicity). Key research efforts that have been accelerated by federal support include the development of high-rate vapor transport deposition, Group V doping, and zinc telluride back contact technology. These innovations have ultimately helped enable high-volume high-throughput CdTe process capability with efficiencies over 19% and long projected lifespans (estimated >25 years).22,23,24,25,26,27 In addition to their direct impacts, these actions collectively have reduced the risk for large-scale investment in CdTe manufacturing technology and accelerated industrial growth.28,29

There are two consortia that are active in CdTe technology development: CTAC, launched by DOE in 2022, is administered by NREL and funds work throughout the domestic CdTe R&D community. This consortium was created in response to specific congressional direction to accelerate domestic CdTe PV and includes key industrial and academic stakeholders. CTAC works toward the goals of CdTe cell efficiencies of > 24% by the end of 2025 and > 26% by the end of 2030, and it periodically releases solicitations for new research projects in areas that are important to the consortium’s goals.

The United States Manufacturing of Advanced Cadmium Telluride (US-MAC) consortium was formed as a result of years of ongoing interaction and collaboration between members of the CdTe R&D community. US-MAC goals include enhancing and expanding the CdTe R&D ecosystem, supporting engagement between its members, and working to improve the overall competitiveness and market share of the CdTe PV technology.

SETO Research Priorities for CdTe Research, Development, and Demonstration

SETO supports innovation to harness America's abundant solar energy resources for secure, affordable, and reliable electricity. As a key part of this mission, SETO seeks to enable a sustainable, robust, and resilient solar supply chain that provides domestic value and job creation. SETO accelerates the expansion of domestic manufacturing capacity and spurs private-sector investment by reducing technical and commercial risk of new technologies. The innovations and technologies that SETO funds increase value and domestic content of solar products across the entire supply chain and ensure U.S. technology leadership. Going forward, SETO will support CdTe PV through programs aimed at the following priority areas.

Improving CdTe Cell and Module Performance

Achieving the highest possible module efficiency remains a major challenge for CdTe technology development, and with silicon PV manufacturers rapidly pivoting toward advanced bifacial and back contact cells that make use of tunnel oxide and heterojunction contact passivation, the race to maximize module performance is likely to become even more intense in the near future.

There are a variety of opportunities in CdTe PV cell and module manufacturing process that can increase PCE.31 For example, improvements in window transparency, dopant activation, minority carrier lifetime, contact selectivity, and band edge defect states may improve PV performance, while thinner glass can reduce light absorption, cycle time, and total embodied energy.

SETO’s support for activities in this area is currently provided through the FY24 Photovoltaics Research and Development FOA, the Advancing U.S. Thin-Film Solar Photovoltaics FOA, and the Materials, Operation, and Recycling of Photovoltaics (MORE PV) FOA. Recent support has also been provided through CTAC’s 2023 Small Projects to Accelerate CdTe Technology Development and the SIPS funding program, as well as NREL core program funding for CdTe research.

Modern CdTe PV modules are generally able to produce favorable energy yields per nameplate watt due in part to their temperature coefficient and blue-light spectral response as compared to silicon PV modules. The copper replacement module technology that is currently under development by First Solar represents one of the lowest warranted power loss rates for any PV cell technology and indicates a high degree of confidence in the expected degradation rates of this new technology.

Two areas where CdTe modules currently lag behind other absorbers are bifaciality and tandem integration. Advanced silicon cell technologies such as those using tunnel oxide and heterojunction architectures can exhibit rear-side efficiencies that are 85% or more of the front-side efficiency. CdTe cells are beginning to demonstrate bifaciality, but at significantly lower levels. Tandem cell architectures are becoming quite common in the long-term roadmaps of major PV manufacturers as cell fabrication costs are reduced and increasing efficiency becomes a larger and more potent lever for reducing the overall cost of PV systems. Silicon, perovskites, and copper indium gallium selenide absorbers have bandgaps that are very well suited for integration into tandem cells, but CdTe is caught in a middle ground that is difficult to optimize around. The incorporation of zinc or magnesium to form cadmium zine telluride (CdZnTe) and cadmium magnesium telluride (CdMgTe) represents a possible way to move the bandgap into a viable regime for tandem incorporation, but using these materials introduces processing challenges that have thus far prevented their use in high-throughput manufacturing. This area of research is open to new solutions and may become important in the medium to long term as tandem cell technologies attempt to enter the mainstream PV market.

SETO’s support for activities in this area is currently provided through the Advancing U.S. Thin-Film Solar Photovoltaics FOA. Recent support has also been provided through the Fiscal Year 2022 Solar Manufacturing Incubator, CTAC’s 2023 Small Projects to Accelerate CdTe Technology Development, and the SIPS funding program.

Increasing Materials Availability and Strengthening the Supply Chain

Tellurium (Te) is a chemical element that makes up 10 to 15% of the cost of a CdTe PV module. Though not seen to date, its constrained availability may place a practical limit on the maximum size of the CdTe PV supply chain. It is difficult to identify this ceiling due to uncertainty in global Te production, which is primarily harvested as a by-product of copper refining. The United States Geological Survey has reported that approximately 640 metric tons of Te were produced globally in 2022,32 although anecdotal reports indicate that the amount of Te available on the international market may be significantly higher. Historically, copper refining processes have been optimized exclusively for copper production, and Te recovery capabilities have not yet been deployed in many relevant copper processing facilities. As Te recovery capabilities are introduced and as global copper production changes in the coming years, the availability of Te will adjust accordingly.

Breakthroughs in the production, refining, or overall availability of Te represent important areas of work due to their ability to significantly increase the maximum possible market size for CdTe PV. More comprehensive implementation of Te recovery capabilities from currently available copper electrorefining residues has been estimated to be capable of substantially increasing global annual Te production, perhaps by a factor of 2–3x.33 Further Te resources that have been identified include the Te that is currently lost during intermediate steps in the copper refining process, and as part of copper and other metal ore mine tailings, which are estimated as having an additional multiplier effect on potential Te availability. Increasing Te production can be challenging since commodity Te is only produced as a by-product of copper refining and is not mined directly.34 New technologies that enable the efficient extraction of larger quantities of Te within the copper refining process are needed. Module EOL management through recycling preserves Te that has been extracted while minimizing the energy needed to reuse this critical mineral refined and incorporated into fielded modules for reuse (vide infra).

SETO’s support for activities in this area is currently provided through the Advancing U.S. Thin-Film Solar Photovoltaics FOA. Recent support has also been provided through CTAC’s 2023 Small Projects to Accelerate CdTe Technology Development.

Improvements in manufacturing efficiency, including innovations in equipment, metrology, and automation, could increase manufacturing scale and deployment. Innovations to further reduce the embodied energy of module components and to enable larger-volume manufacturing of CdTe PV modules and their components across the supply chain will support increased deployment of this technology. The entire set of materials comprising CdTe PV and the process used to integrate them impacts the cost and lifetime performance of the technology. Improvements to the lifetime performance can decrease the LCOE; however, long-term field validation studies are needed to quantify the value.

Glass advances that can reduce weight or increase supply have the potential to reduce cost. One example is integration of thinner glass superstrates. A 33% reduction in glass thickness (3 millimeter to 2 millimeter) can yield 50% more modules with the same input energy and reduces the shipping weight of finished modules (and therefore embedded energy from glass) by nearly 15%. This also improves throughput and reduces the energy required in all unit processes where the glass is heated and cooled. The operational expenses as well as energy savings should translate to lower manufacturing cost.

SETO’s support for activities in this area is currently provided through the Advancing U.S. Thin-Film Solar Photovoltaics FOA. Recent support has also been provided through the Solar Manufacturing Incubator FOA and the American-Made Solar Prize.

Enabling Large-Scale Deployment and End-of-Life Reclamation

With increasing CdTe PV deployment, innovations in plant and fleet monitoring and diagnostic methods can improve the reliability and reduce the cost of this technology at scale. System operators and operations and maintenance firms that are accustomed to silicon PV modules may need additional information and resources to begin making use of CdTe PV modules. New system monitoring and maintenance approaches developed specifically for CdTe PV systems along with the adaptation to CdTe of best practices currently used on c-Si PV systems can help maximize value and enable even larger-scale deployment of the CdTe PV technology.

SETO’s support for activities in this area is currently provided through the Advancing U.S. Thin-Film Solar Photovoltaics FOA and through the MORE PV FOA.

First Solar’s planned manufacturing expansions will place significant demands on the local workforce in order to successfully build and staff the intended production facilities. A similar build-out of manufacturing capacity across the silicon supply chain will require similarly capable workers to produce the PV modules needed to meet domestic demand. SETO has an established priority to support the training and advancement of a skilled workforce that is representative of their local communities and of the larger national population. Historically these efforts have been focused on augmenting the downstream workforce that deploys and operates PV systems, but the recent explosion of manufacturing announcements that have followed the IRA and Creating Helpful Incentives to Produce Semiconductors Act has created uncertainty about whether there will be sufficient workers available to build and staff the intended production facilities.

SETO is currently developing its plans to assist in training the U.S. PV manufacturing workforce, and the Scaling the U.S. Solar Manufacturing Workforce Request for Information was previously released to determine the most effective ways to support work in this area. Recent support has also been provided through the Solar Manufacturing Incubator FOA and the American-Made Upskill Prize for the Solar Manufacturing Workforce.

As the number of deployed CdTe systems grows and the fleet ages, EOL planning becomes increasingly important. As CdTe PV modules approach their eventual decommissioning, it is generally the responsibility of the system owners to ensure that modules are recycled or disposed of in compliance with any applicable regulations. SETO wants to help enable every CdTe PV module to be disposed of according to any applicable regulations, and to improve recycling technology so the component materials can be recaptured by the domestic supply chain. Given that millions of PV modules are deployed every year, it will be a significant challenge to successfully return them to recycling facilities for processing. New ideas or technologies that can assist with this goal are also of potential interest for future RD&D efforts.

Reclamation and recycling of CdTe PV materials that are eventually decommissioned from the field can also help extend the availability of Te, although this material stream will be delayed by the significant service lifetime of typical PV modules. Other materials used in modules, such as aluminum, steel, selenium, and glass, are also potentially recyclable. Innovations in CdTe PV recycling processes and their automation can further reduce waste and cost and improve materials availability. CdTe module recycling technology has already been demonstrated by First Solar at moderate scale and has the potential for further innovation. While manufacturing scrap is recycled on-site, EOL CdTe modules are currently primarily landfilled, as it is currently much cheaper than recycling.

SETO’s support for activities in this area is currently provided through the Advancing U.S. Thin-Film Solar Photovoltaics FOA and the MORE PV FOA.

Additional Resources

- Download the full CdTe PV Perspective Paper (PDF).

- Dive into SETO’s work on cadmium telluride.

- Explore SETO’s research in photovoltaics and manufacturing and competitiveness.

- Learn about SETO’s goals.

Endnotes

1Smith, B. L., A. Sekar, H. Mirletz, G. Heath, and R. Margolis. 2024. An Updated Life Cycle Assessment of Utility-Scale Solar Photovoltaic Systems Installed in the United States. NREL. www.nrel.gov/docs/fy24osti/87372.pdf.

2Feldman, D., K. Dummit, J. Zuboy, and R. Margolis. 2023. Summer 2023 Solar Industry Update. NREL. www.nrel.gov/docs/fy23osti/87189.pdf.

3Feldman, D., J. Zuboy, K. Dummit, D. Stright, M. Heine, S. Grossman, and R. Margolis. 2024. Spring 2024 Solar Industry Update. NREL. www.nrel.gov/docs/fy24osti/90042.pdf.

4Feldman, D., K. Dummit, J. Zuboy, and R. Margolis. 2023 Spring 2023 Solar Industry Update. NREL. www.nrel.gov/docs/fy23osti/86215.pdf.

5See, for example, 5N Plus Inc. 2024. “5N Plus Inc. Renews and Increases Semiconductor Supply Agreement with First Solar.” www.5nplus.com/en/news/5n-plus-inc-renews-and-increases-semiconductor-sup/;

Department of Defense. 2024. “DOD Awards $14.4 Million to Sustain and Enhance the Space-Qualified Solar Cell Supply Chain.” www.defense.gov/News/Releases/Release/Article/3743467/dod-awards-144-million-to-sustain-and-enhance-the-space-qualified-solar-cell-su/; Lasley, S. 2022. “First Solar Powers New Tellurium Demand.” Metal Tech News. https://www.metaltechnews.com/story/2022/09/12/critical-minerals-alliances-2022/first-solar-powers-new-tellurium-demand/1082.html.

6Wikoff, H. M., S. B. Reese, and M. O. Reese. 2022. “Embodied Carbon from the Manufacture of Cadmium Telluride and Silicon Photovoltaics.” Joule. doi.org/10.1016/j.joule.2022.06.006.

7Id.

8Green, M., Dunlop, E., Yoshita, M., Kopidakis, N., Bothe, K., Siefer, G., Hao, X. and Jiang, J. (2024), Solar Cell Efficiency Tables (Version 65). Prog Photovolt Res Appl. https://doi.org/10.1002/pip.3867

9Scarpulla, M. A., et al. 2023. “CdTe-Based Thin Film Photovoltaics: Recent Advances, Current Challengesand Future Prospects.” Solar Energy Materials and Solar Cells. https://www.sciencedirect.com/science/article/pii/S0927024823001101.

10Di Sabatino, M., R. Hendawi, and A. S. Garcia. 2024. “Silicon Solar Cells: Trends, Manufacturing Challenges, and AI Perspectives.” Sustainable Energy Technology. www.mdpi.com/2073-4352/14/2/167.

11WTOL. 2024. “Toledo Solar to Close, Citing Challenges With Production and Lack of Cooperation From Other Companies.” www.wtol.com/article/news/local/toledo-solar-to-close-challenges-production-lack-of-cooperation-from-companies/512-c73ac155-b479-4447-b2a5-28cbb4f5e8dd.

12First Solar. 2024. U.S. Securities and Exchange Commission Form 10-Q. https://s202.q4cdn.com/499595574/files/doc_financials/2024/q3/4aa851ff-d2b9-465c-9eae-20806ac61e81.pdf.

13First Solar. 2024. “First Solar Inaugurates $1.1 Billion Alabama Facility, Adds 3.5 GW of Vertically Integrated American Solar Manufacturing Capacity.” https://investor.firstsolar.com/news/news-details/2024/First-Solar-Inaugurates-1.1-Billion-Alabama-Facility-Adds-3.5-GW-of-Vertically-Integrated-American-Solar-Manufacturing-Capacity/default.aspx.

14Vitro. 2023. “Vitro Enters Into Agreement With First Solar for the Manufacture of Glass for American-Made Solar Panels.” www.vitroglazings.com/about/news/vitro-enters-into-agreement-with-first-solar-for-the-manufacture-of-glass-for-american-made-solar-panels/.

15Smith, B. L., M. Woodhouse, K. A. W. Horowitz, T. J. Silverman, J. Zuboy, and R. M. Margolis. 2021. Photovoltaic (PV) Module Technologies: 2020 Benchmark Costs and Technology Evolution Framework Results. NREL. www.nrel.gov/docs/fy22osti/78173.pdf.

16In addition, there is a case pending for four southeast Asian countries: International Trade Administration. “Commerce Initiates Antidumping and Countervailing Duty Investigations of Crystalline Silicon Photovoltaic Cells from Cambodia, Malaysia, Thailand, and the Socialist Republic of Vietnam.” www.trade.gov/commerce-initiates-antidumping-and-countervailing-duty-investigations-crystalline-silicon.

17Internal Revenue Service. www.irs.gov/credits-and-deductions-under-the-inflation-reduction-act-of-2022.

18SETO. Cadmium Telluride. www.energy.gov/eere/solar/cadmium-telluride.

19SETO. Solar Research and Development Funding Programs. www.energy.gov/eere/solar/solar-research-and-development-funding-programs.

20NREL. 2023. “News Release: NREL Awards $2 Million in Contracts To Support Development of Cheaper, More Efficient Cadmium Telluride Solar Cells.” www.nrel.gov/news/press/2023/news-release-nrel-awards-2-million-in-contracts-to-support-development-of-cheaper-efficient-cadmium-telluride-solar-cells.html.

21NREL. Cadmium Telluride Solar Cells. https://www.nrel.gov/pv/cadmium-telluride-solar-cells.html.

22NREL. 2013. “Rapid Deposition Technology Holds the Key for the World’s Largest Manufacturer of Thin-Film Solar Modules.” www.nrel.gov/docs/fy13osti/59010.pdf.

23Burst, J. M., et al. 2016. “CdTe Solar Cells With Open-Circuit Voltage Breaking the 1 V Barrier.” Nature Energy. www.nature.com/articles/nenergy201615.

24Gessert, T. A., et al. 1997. “Studies of ZnTe Back Contacts to CdS/CdTe Solar Cells.” NREL. www.nrel.gov/docs/legosti/fy97/22983.pdf.

25First Solar. 2023. “Series 6 Plus Bifacial.” www.firstsolar.com/-/media/First-Solar/Technical-Documents/Series-6-Plus/Series-6-Plus-Bifacial-Datasheet---US.ashx?la=en.

26NREL. 1996. “Stability Testing of CdTe/CdS Thin-Film Photovoltaic Modules.” https://research-hub.nrel.gov/en/publications/stability-testing-of-cdtecds-thin-film-photovoltaic-modules.

27NREL. 2020. “First Solar’s Photovoltaic Technology Completes 25 Years of Testing at NREL.” www.nrel.gov/news/program/2020/first-solars-photovoltaic-technology-completes-25-years-testing-at-nrel.html.

28Cheese, E., M. K. Mapes, K. M. Turo, R. Jones-Albertus. 2016. “U.S. Department of Energy Photovoltaics Research Evaluation and Assessment.” ieeexplore.ieee.org/document/7750314.

29Engel-Cox, J. A., et al. 2022. “Clean Energy Technology Pathways From Research to Commercialization: Policy and Practice Case Studies.” Frontiers in Energy Research. www.frontiersin.org/articles/10.3389/fenrg.2022.1011990/full.

30SETO. Manufacturing and Competitiveness. www.energy.gov/eere/solar/manufacturing-and-competitiveness.

31Scarpulla, M. A., et al. 2023. “CdTe-Based Thin Film Photovoltaics: Recent Advances, Current Challenges and Future Prospects.” Solar Energy Materials and Solar Cells. www.sciencedirect.com/science/article/pii/S0927024823001101.

32U.S. Geological Survey. 2023. “Tellurium.” pubs.usgs.gov/periodicals/mcs2023/mcs2023-tellurium.pdf.

33Nassar, N. T., H. Kim, M. Frenzel, M. S. Moats, and S. M. Hayes. 2022. “Global Tellurium Supply Potential From Electrolytic Copper Refining.” Resources, Conservation and Recycling. www.sciencedirect.com/science/article/pii/S0921344922002774.

34McNulty, B. A., and S. M. Jowitt. 2022. “Byproduct Critical Metal Supply and Demand and Implications for the Energy Transition: A Case Study of Tellurium Supply and CdTe PV Demand. Renewable and Sustainable Energy Reviews. www.sciencedirect.com/science/article/abs/pii/S1364032122007213.

35U.S. Geological Survey. 2022. “2022 Final List of Critical Minerals.” www.federalregister.gov/documents/2022/02/24/2022-04027/2022-final-list-of-critical-minerals.