Updates to DOE's Pathways to Commercial Liftoff: Advanced Nuclear Report

September 30, 2024The nuclear energy landscape in the United States is changing rapidly as demand for clean firm power rises and the nation strives to meet its climate goals.

Thanks to the Bipartisan Infrastructure Law and Inflation Reduction Act, the domestic nuclear industry is leveraging federal funding, loan authority, and new tax incentives to extend reactor operations, increase capacity, and restart our retired reactors.

Early last year, the U.S. Department of Energy (DOE) released a report on how to commercialize advanced nuclear technologies and they've now updated it to generate faster, more coordinated action for the deployment of advanced reactors so we can increase our access to clean energy.

Here’s what’s new.

Meeting Surging Demand

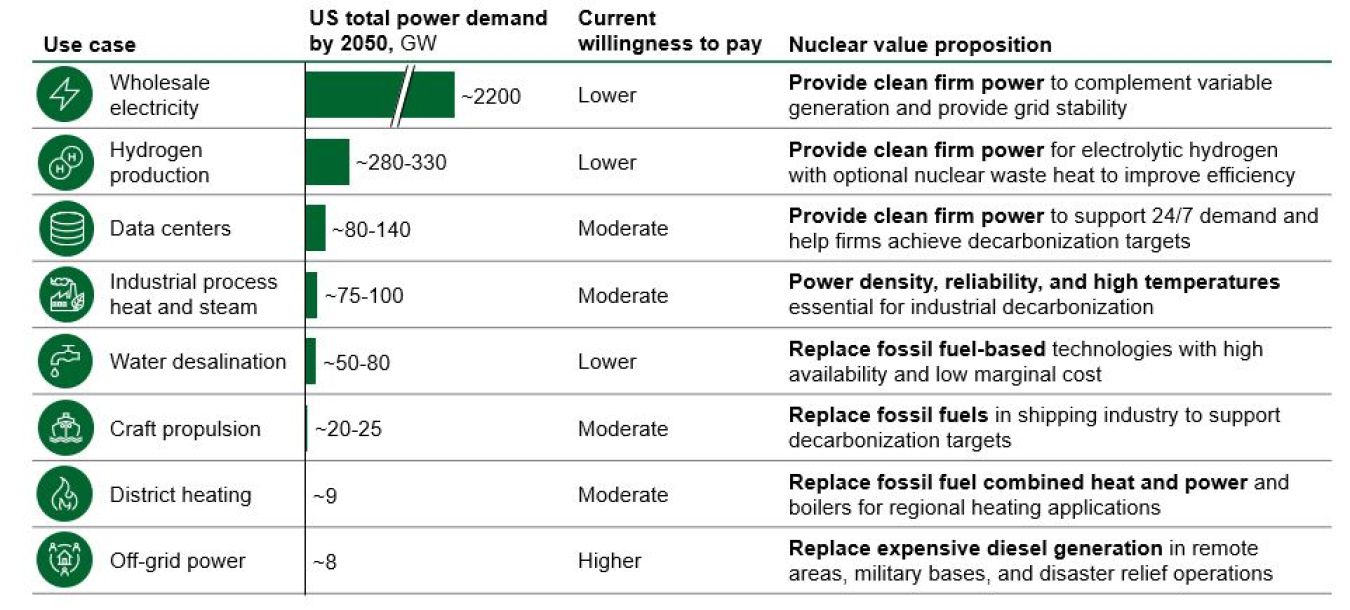

The updated report finds that the United States will now need at least 700 to 900 gigawatts (GW) of additional clean firm power to keep pace with updated load growth projections to reach net-zero emissions.

This surge in electricity demand is driven partly by data centers for artificial intelligence and high-performance computing, which could increase the total power demand by up to 20% next decade.

Nuclear is one of the few options that can reliably deliver at this scale.

Data centers require firm power for around-the-clock operations, and many large technology companies are already leaning into nuclear power as a solution as well as other potential use cases explained in the chart below.

Tripling Nuclear Capacity

The United States joined more than 20 other nations last year in pledging to triple nuclear energy capacity globally by 2050.

Together, they committed to supporting the development and construction of nuclear reactors, mobilizing investments in nuclear power, promoting resilient supply chains, and recognizing the importance of extending the lifetimes of existing nuclear power plants.

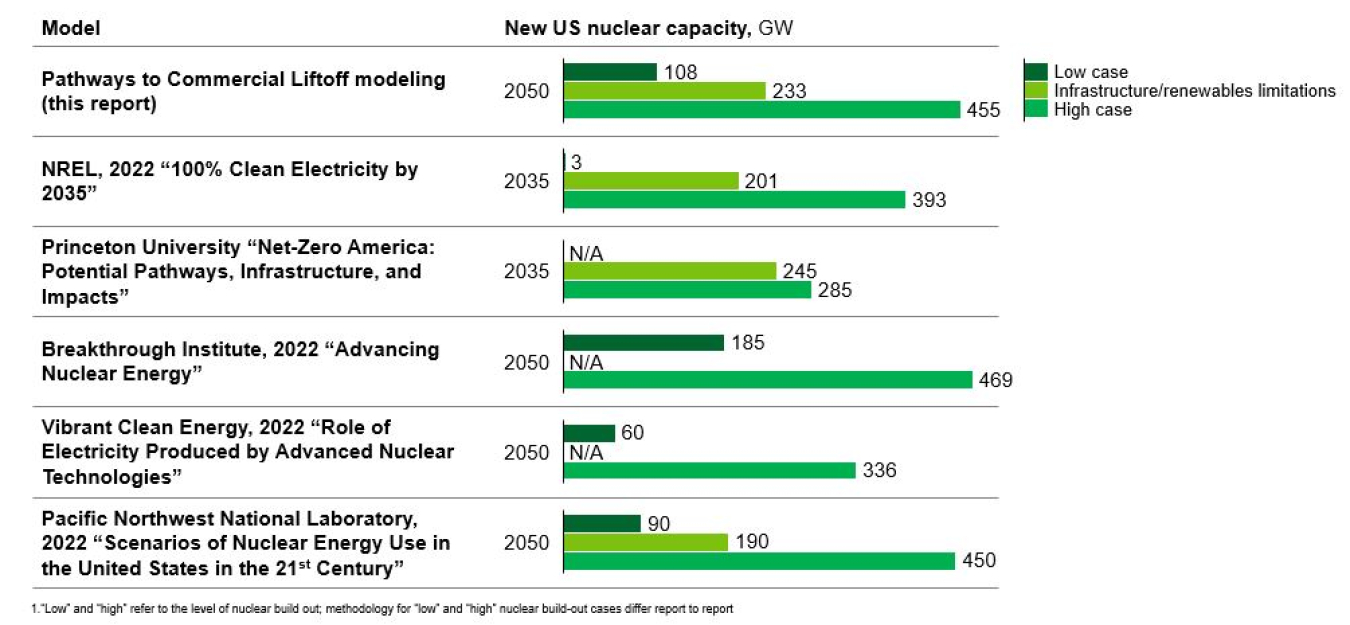

According to the report, U.S. nuclear capacity has the potential to triple to ~300 GW by 2050.

Preliminary research cited in the report also shows that a substantial amount of the new capacity could come at existing and recently retired nuclear power plant sites. DOE found that 41 sites have room to host one or more large light-water reactors, such as the AP1000 reactors recently built at Plant Vogtle in Georgia, which would create an additional 60 GW of new capacity.

This number could grow to 95 GW if you look at sites that can potentially host smaller, advanced reactors of up to 600 MW.

Coal plants are another potential venue for new reactor construction.

Research indicates that an additional 128 to 174 GW of new nuclear capacity could be built near coal plants — many of which are projected to retire by 2035 as states transition to cleaner energy sources.

Lessons Learned from Recent Builds

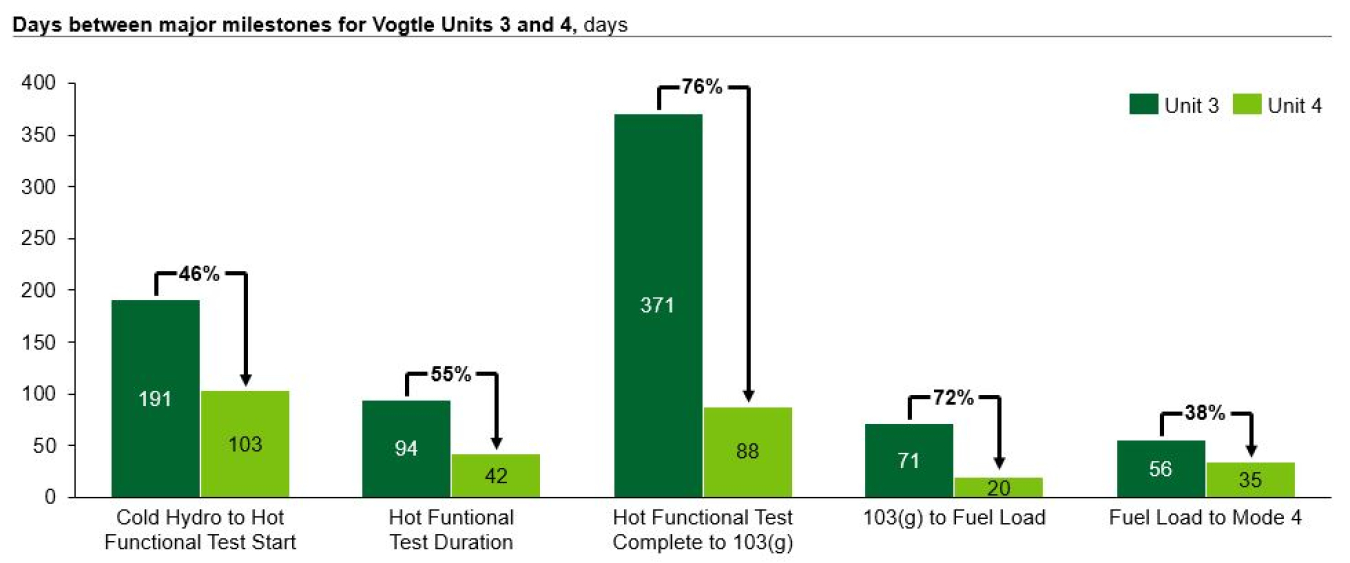

The nuclear industry is building momentum after the completion of Vogtle Units 3 and 4, which were boosted by the demand for clean energy and availability of federal tax credits that can be paired with attractive debt financing from our Loan Programs Office.

As a result, Plant Vogtle is the largest generator of clean electricity in the United States!

To sustain this momentum, the industry must learn from Vogtle’s construction and ensure that future projects are completed on time and on budget.

The report explains that many of Vogtle’s cost were first-of-a-kind or project-specific costs that would be unlikely to repeat with the next AP1000s.

This is because Vogtle began construction with an incomplete AP1000 design, an immature supply chain, and an untrained work force.

Now the AP1000 design is complete, the supply chain infrastructure has been built, and more than 30,000 workers have been trained.

Just take a look at the improvements made from Vogtle Unit 3 to Unit 4 across key milestones in the project.

The report explains that Unit 4 is estimated to have been roughly 30% more efficient and 20% cheaper to build than Unit 3, and future reactor projects can expect to see even greater savings!

The Value of a Consortium

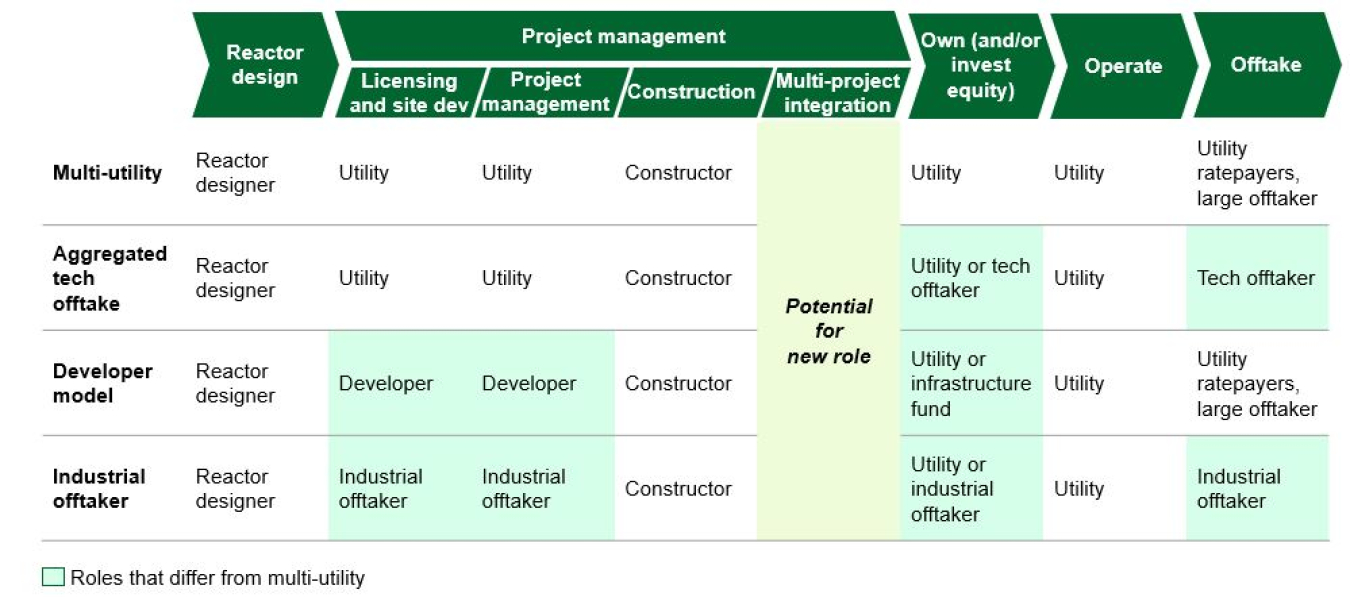

The report also shows how the nuclear industry would benefit from adopting consortium approaches to nuclear reactor construction.

Building a “first-of-a-kind” nuclear reactor is almost always more expensive than the second or third. By working together in a consortium, customers looking to buy nuclear reactors can spread the early costs across all participants and share the savings as additional units are delivered.

Many roles need to be filled for a nuclear project: reactor design, project development, owning, operating, and offtake.

The chart below highlights these different roles and how each role could be filled under different consortium approaches.

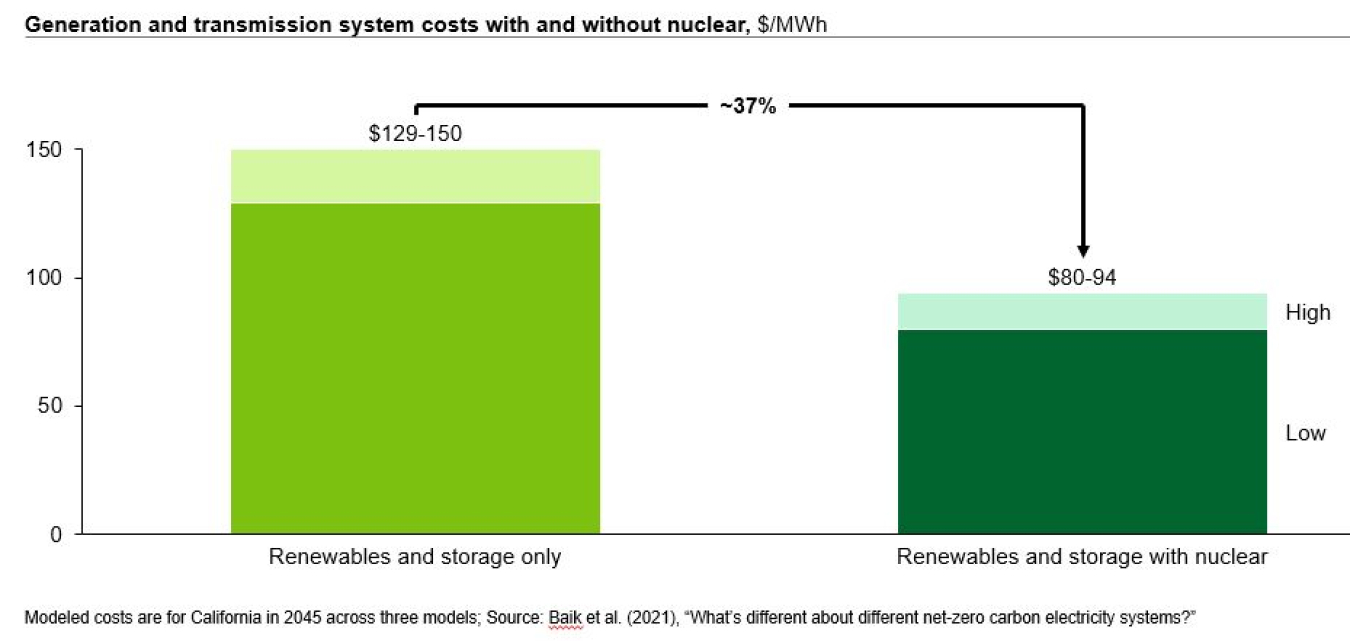

Nuclear Complements Renewable Energy Sources

Finally, another key takeaway from the report is that building nuclear power plants along with renewables and storage is actually a cheaper way to decarbonize the grid than just nuclear or renewables alone.

Nuclear energy can provide clean electricity during the most expensive hours when wind and solar are unavailable and also reduces the amount of generation capacity, storage, and transmission needed to ensure grid reliability.

A diverse mix of clean firm generation, variable renewables, and energy storage creates the most cost-effective system.

Across multiple power system models, pairing renewables and storage with nuclear energy could lead to a ~37% reduction in generation and transmission system costs.

Dr. Michael Goff

Dr. Michael Goff is the Principal Deputy Assistant Secretary for the U.S. Department of Energy’s Office of Nuclear Energy. Prior to joining the office as the PDAS, Dr. Goff was on assignment from Idaho National Laboratory (INL) to the Office of Nuclear Energy, where he was serving his third term as senior advisor to the Assistant Secretary. Dr. Goff also served a multi-year assignment as the assistant director for Nuclear Energy/Senior Policy Advisor in the Office of Science and Technology Policy in the Executive Office of the President. He has held several management and research positions over more than 30 years at INL and Argonne National Laboratory.

Dr. Goff has more than 70 publications related to the nuclear fuel cycle including separations technology, high-level waste development, and safeguards. Dr. Goff has a bachelor's degree of nuclear engineering (1986), a MSNE (1988), and a Ph.D. in nuclear engineering (1991), all from Georgia Tech.